Why I like Alphabet more than Apple — and Buffett doesn’t

Alphabet (better known as Google), with a market cap of $856 billion, trails only Apple ($948 billion) in the race to be the first company to achieve a market cap of $1 trillion. Apple will likely get there first but my money — unlike my investing hero, Warren Buffett — is on Alphabet significantly outperforming Apple in the long run because it has a better business model, is growing much faster, and is likely to continue doing so.

Both are great companies

To be clear, both are insanely great companies and I think Apple’s stock will also do well going forward — just not as well as Alphabet’s.

Apple’s virtues are well-known: It makes tremendous products, especially the iPhone, which accounts for two-thirds of its revenues, and has intensely loyal customers. While iPhones only accounted for 15.6% of all smartphones sold globally in Q1 2018, their premium pricing allowed Apple to earn nearly 90% of all profits in the sector.

Alphabet is also a tremendous business. It has large, sustainable competitive advantages in the form of brands, habits, and network effects, and has a low-capital-intensive, high-margin business model that generates gobs of free cash flow. It has seven products with more than 1 billion monthly average users: Search, Android, Maps, Chrome, YouTube, Google Play and Gmail. Google Search has 90% share of search in most countries, Android has 86% share of smartphones globally, and YouTube serves 20% (and growing) of all video consumed on the internet. Alphabet currently captures 15% of global advertising spending, and 100% of the incremental ad spending in the world is going to Alphabet and Facebook.

Apple has a fabulous business model, but Alphabet’s is even better in my opinion. Apple actually has to do things: develop and have manufactured a physical product, ship it all over the world, carry inventory, operate stores, etc. And its business model has some real risks: At its core, Apple is a device maker. And the tech world is littered with the carcasses of failed device makers like Palm, Motorola, Nokia and Research in Motion.

In contrast, Alphabet’s business is information and it only has to deliver electronic bits and bytes, so it can expand to serve every human on earth at virtually zero incremental cost.

Just think about it: One company make a fabulous gadget, while the other puts all human knowledge at your fingertips in milliseconds. Which one do you think is going to grow faster and be bigger in the coming years?

Or here’s another way to think about it: In 10-20 years, what are the odds that my children and grandchildren will be using Apple’s products? I’d guess 75%. And Alphabet’s? 95%+.

Historical growth rates

Alphabet has been showing much faster and steadier growth than Apple. It just reported another blowout quarter, with year-over-year revenue growth exceeding 25% — its 9th consecutive quarter of 20%+ revenue growth — as this chart shows:

It’s extraordinary that a company of this size — its revenue run rate exceeds $130 billion — is growing this rapidly. And it’s accelerating.

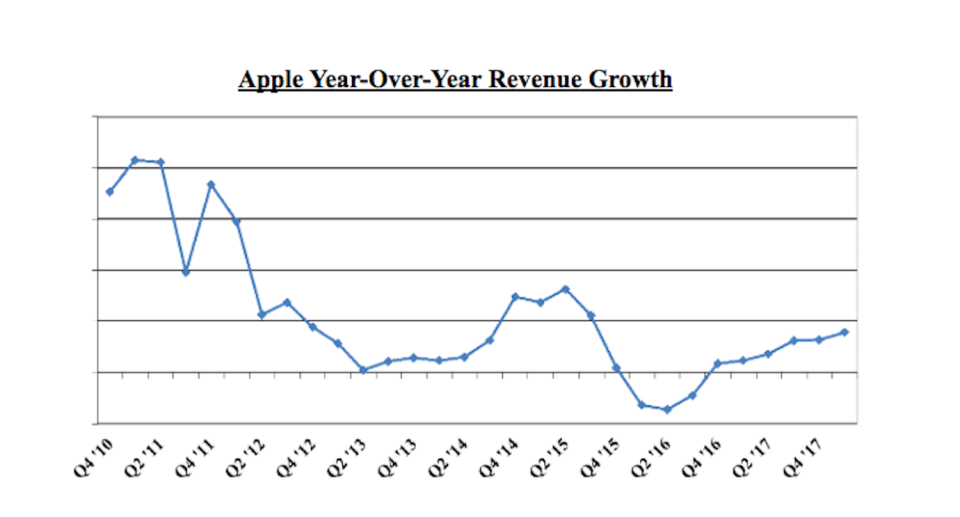

In contrast, in the last 22 quarters — 5½ years — Apple has only had four quarters of 20% revenue growth (and three quarters of revenue declines), as this chart shows:

Growth has picked up in the last year and a half, but is quite a bit below Alphabet’s.

Future growth

How well each of these stocks does going forward, however, isn’t a function of historical growth, but rather future growth (among other factors) — and here I think Alphabet has a big edge, as well.

For starters, size is an anchor and Alphabet is starting from a much lower base, with half the revenues of Apple.

And there is plenty of room for growth, as Alphabet is benefitting from three huge trends: advertising moving from traditional media to online, more commerce moving online (only ~12% of U.S. commerce is online today), and increasing smartphone penetration (it’s only ~32% globally today).

Of the two-thirds of all adults on earth who don’t currently have a smartphone, most will get one in the coming years. At first glance, this would seem to favor Apple over Alphabet — but I disagree. Those who don’t have smartphones currently are generally low-income, and Apple has very few inexpensive products. My view is that pretty much everyone who can afford an iPhone already has one, so where will growth come from (especially since I haven’t seen much innovation from Apple in the post-Steve Jobs era)?

Meanwhile, Alphabet, led by its seven products with over 1 billion users per month, stands to be the primary beneficiary of a few billion more people getting smartphones.

Valuation

Another big factor that will determine each of these stocks’ future performance is current valuation. Apple has an edge here, but it’s not as big as it seems.

Apple’s stock trades at 16.8 times this year’s consensus earnings estimates (14.1 times if you exclude $31/share of net cash) vs. a bit over 25 times for Alphabet (after a blowout Q2, analysts’ estimates will surely be going up a lot).

But Alphabet’s stock is only trading for roughly 20 times 2018 earnings estimates if you subtract net cash ($140/share) and the value of Other Bets (I conservatively estimate $50/share), and add $2.7 billion ($3.89/share) to net income for after-tax losses on Other Bets.That’s not far above the average for the S&P 500, for a company that is vastly superior to the average large U.S. corporation.

Here’s a very simple way that I think about what I think I’m likely to earn from owning Alphabet’s stock: If revenues continue to grow at ~20% annually for the next 3-5 years and margins and multiples remain steady, then the stock will also grow at ~20% annually. That’s just simple math. You just have to be right on the three assumptions, and I think they’re reasonable.

Doing the same back-of-the-envelope exercise for Apple, I think revenues will grow closer to 10% annually and I also think margins and multiples will remain steady, resulting in the stock appreciating 10% per year. Even if you add in a 1.6% dividend and share repurchases, that doesn’t get you anywhere close to the 20% annual return I expect from Alphabet.

In summary, when it comes to growth-oriented tech stocks, it’s growth, not cheapness, that matters — and I think Alphabet has much more growth ahead of it than Apple.

So why does Buffett own $46 billion of Apple and $0 of Alphabet?

As a Berkshire shareholder for the last two decades, I’m not unhappy that Warren Buffett owns $46 billion of Apple stock because I think it will compound nicely. But I do wish he owned, say, $30 billion of Alphabet and $16 billion of Apple, as I think Alphabet’s stock is perhaps 75% likely to do better than Apple’s over any 3+ year time horizon for the reasons outlined above.

So why did Buffett buy Apple’s stock instead of Alphabet’s? I think there are a variety of reasons. First and foremost, its stock is quite a bit cheaper on a current year earnings multiple basis. Second, he likes the big return of capital to shareholders (mostly in the form of share repurchases). Third, it’s easier for him to get comfortable with it from a circle of competence perspective.

In general, he doesn’t like tech because it’s difficult to understand and hard to predict the future. But Apple is more like a consumer products company, with products that Buffett can see and touch. Fourth, it’s easier to understand the moat around Apple’s business (though I actually think Alphabet’s is bigger and will prove to be more enduring).

And lastly, Buffett may be suffering a bit from the “I missed it” phenomenon, as he and Charlie Munger have engaged in self-flagellation recently for missing the stock many years ago.

It’s so hard for a value investor to look at a stock, not buy it, watch it go up a lot — and then buy it. But in this case, that’s what I’m doing — and I think Buffett should as well.

(For more on our analysis of Alphabet and Facebook, see: http://www.tilsonfunds.com/TilsonGOOGFB.pdf.)

Whitney Tilson founded and for nearly two decades managed hedge fund Kase Capital. He is now teaching the next generation of investors via his new business, Kase Learning.

Read more: